I'm a computer programmer. I write code for a living — backend systems, cloud infrastructure, the kind of work that keeps enterprise software running. I am not a licensed financial advisor. I'm not a Wall Street trader. I don't have an MBA or a Series 7 or any credential that says I'm qualified to talk about money.

What I do have is a CNBC habit. Squawk Box before my morning standup. Jim Cramer on Mad Money after dinner. And a growing, uncomfortable awareness that the tools I use to be productive — Claude, Copilot, ChatGPT — are the same tools that will eventually make me replaceable.

I don't say that with self-pity. I say it because it's the reason I started looking for income streams that don't depend on an employer deciding I'm still worth paying.

Like a lot of people, I started by researching "real" businesses. Vending machines. Run-down laundromats I could fix up. Maybe a franchise. Something I could build on the side that would keep generating income whether or not my W-2 survived the next round of AI-driven layoffs.

The vending machines looked okay on paper. Buy a few machines, find good locations, stock them, collect cash. But then I thought about what that actually looked like: driving around town restocking chips and drinks, negotiating with strip mall managers for floor space, dealing with jammed coin slots. And the exit? If I ever wanted out, I'd have to sell the machines to someone — probably at a fraction of what I paid. That didn't feel like freedom. It felt like a second job with worse hours.

Laundromats were the same story in a bigger package. The "buy a run-down one and renovate it" strategy sounds brilliant on real estate podcasts. In reality, it means bank loans, contractors, plumbing nightmares, and being on call when a washer floods at 10 PM. I didn't want a bank loan. I didn't want to be on call. I wanted income that ran without me.

Then something clicked.

I already owned stocks. A small portfolio — nothing impressive. I started reading about selling options, specifically covered calls and cash-secured puts. I watched a few YouTube videos. I spent too many hours on Reddit's r/thetagang. And one afternoon, I sold my first covered call.

The premium — maybe $40 — hit my brokerage account that same day. No customer. No product. No delivery. No location. No employee. Just capital and a decision.

That was the moment I realized: this is a business.

Why I Think of This as a Business, Not a "Side Hustle"

Every business requires startup capital. A food truck costs $50,000 to $100,000. A franchise runs $25,000 to $500,000. A laundromat costs $200,000 or more. Even a modest vending route will set you back $5,000 to $10,000 before you see your first dollar.

My business cost me under $5,000 to start. That's the price of 100 shares of two stocks I believe in. That's my entire startup cost — no loans, no investors, no Kickstarter campaign.

Every business generates revenue. Mine generates weekly premium income. Real cash, deposited into my brokerage account, every time I sell a contract. The revenue depends on market conditions, the strikes I choose, and which stocks I'm holding — just like any business depends on the market it operates in. I'm not going to throw out fantasy numbers. I recently deployed $6,800 across two positions, and I'm targeting up to $200 a week. That's $10,400 a year — not life-changing on its own, but this is the start, not the finish.

Every business has a growth plan. Mine is simple: take the premiums I collect and buy more shares. More shares means I can sell more contracts. More contracts means more premium. The business funds its own expansion. I don't need to take out a loan to grow. I don't need to hire anyone. I just reinvest the income and the wheel gets bigger.

Here's why this matters if you're a knowledge worker watching AI reshape your industry.

If you're a programmer, a designer, an analyst, a writer — your labor is getting cheaper by the quarter. AI makes one person do the work of three. Employers notice. They always notice.

Labor-based income has a ceiling and a vulnerability. You can only work so many hours, and the value of those hours is being compressed by technology. Capital-based income is different. It doesn't care if GPT-7 can write better code than you. It doesn't care about your job title, your performance review, or your employer's headcount targets.

The covered call business runs on two things: capital and a few minutes of decision-making per week. AI can't replicate your capital. It can't take your shares. It can't collect your premiums.

I'm building income that doesn't depend on anyone deciding my skills are still worth paying for.

The Wheel Strategy in 60 Seconds

If I can learn this as a programmer with zero finance background, you can too. Here's the entire strategy.

1

You promise to buy 100 shares of a stock at a specific price. Someone pays you cash — called premium — for making that promise. If the stock stays above your price by expiration, the contract expires worthless and you keep the cash. You made money for doing nothing but waiting. Repeat.

2

Sometimes the stock drops below your strike price and you have to buy those 100 shares. This isn't a disaster — you chose this stock because you want to own it. You picked the price you were comfortable paying. And the premium you already collected reduces your actual cost.

3

Now you own shares. You promise to sell them at a higher price. Someone pays you premium for that promise. If the stock stays below your strike price, the call expires worthless and you keep both the shares and the premium.

4

If the stock rises above your call strike, your shares are sold — at a profit. You keep the premium plus the capital gain. Now you're back to cash, ready to start at Step 1 again.

That's the wheel. You cycle between selling puts and selling calls, collecting premium at every step. You get paid while you're waiting to buy. You get paid while you're holding. You get paid when you sell. Both sides of the trade generate income.

I didn't learn this in a finance class. I learned it from YouTube, Reddit's r/thetagang, and getting it wrong a few times. You don't need credentials. You need capital, a plan, and the patience to be boring.

Because that's what this strategy is — boring. Repetitive. Methodical. There's no adrenaline rush, no moonshot plays, no diamond hands. Just a small amount of premium hitting your account week after week, like clockwork.

That's exactly why it works.

From Vending Machines to $1K a Week

Let me tell you how this actually happened.

I spent months researching small businesses. Real months — not a weekend Google session. I made spreadsheets. I ran projections. I drove past laundromats and counted how many cars were in the parking lot. I called vending machine distributors and asked about placement fees.

The vending machines would have cost $3,000 to $5,000 per machine, plus location fees, product inventory, and gas money to service them. The revenue projections were $200 to $400 per machine per month — before expenses. And when I eventually wanted to move on? I'd need to find a buyer. Someone who wanted to inherit my routes, my machines, my maintenance schedule. The thought of that conversation exhausted me.

The laundromats were worse. A "fixer-upper" laundromat in my area was listed at $180,000. The seller wanted someone to take over the lease, replace the aging washers, and deal with the property management company. I'd need a bank loan. I'd need to show up. I'd need to care about plumbing.

I didn't want to care about plumbing.

So I stepped back and asked a different question: what if the business was just capital and decisions? No inventory. No locations. No customers. No plumbing. Just money working to create more money.

I was already investing in stocks. Small positions — a few thousand dollars across a handful of companies I followed. I started selling covered calls on shares I already owned. The first week, I made $40. The next week, $65. The week after that, $90.

It wasn't life-changing money. But it was the cleanest income I'd ever earned. No commute. No client. No deadline. Just a decision on my phone and cash in my account.

I started building a plan. What if I could get to $1,000 a week? That's $52,000 a year in premium income. Not by working more hours — by deploying more capital. Every premium I collected went right back into buying more shares, which let me sell more contracts, which generated more premium. The wheel feeds itself.

That's where I am now — scaling toward $1,000 a week. My future target is $2,000. And every dollar of premium I earn is fuel for the next contract.

I don't have a storefront. I don't have employees. I don't have a logo on a van. But I have a business that generates thousands a month, and it takes me five minutes a week to run from my phone.

And if AI replaces my programming job tomorrow, this business keeps running. It doesn't care about my job title. It runs on capital, not credentials.

You Don't Need NVIDIA Money

Here's the objection I hear most: "Don't I need $50,000 to do this?"

If you want to sell puts on NVIDIA at $178.10 a share, you'd need $17,810 per contract. Tesla at $346.65? That's $34,665. For most people, those numbers are a non-starter. And here's the part that rarely gets mentioned: all that capital buys you roughly $100 to $150 a week in covered call premium — nearly the same as what I'm collecting on Planet Labs at $35 a share with $3,600 deployed. You're tying up 5–10× more money for the same weekly income. Bigger names, same paycheck, far less capital efficiency.

But here's what most options content won't tell you: there are dozens of quality stocks under $50 a share that offer weekly options, high implied volatility, and enough premium to build real income. You don't need mega-cap money. You need the right stocks.

Here's what I look for:

- Price per share under $50. Since every options contract controls 100 shares, a $25 stock means $2,500 in capital per contract. A $35 stock means $3,500. That's the range where an average person can start without draining their savings.

- Weekly options available. Not all stocks offer weekly expirations. This is non-negotiable — weekly contracts let you generate income every single week instead of waiting for monthly cycles.

- High volatility momentum. Higher implied volatility means higher premiums. A stock that moves gives you more opportunities and better payouts on every contract you sell. Boring, flat stocks don't generate enough premium to make this worthwhile.

- Tight bid-ask spreads. You don't want to give up a chunk of your premium just getting in and out of the trade. Tight spreads mean liquid options chains.

- A stock you'd actually want to own. This is the most important one. If you get assigned, you're holding 100 shares. You need to be comfortable with that — for weeks or months. Pick companies you believe in.

My Most Recent Acquisitions

These are my actual positions. Real capital, real numbers.

APLD peaked above $35 in late 2024, then pulled back hard. I bought at $32 on the way down — not ideal timing, but the stock has stabilized and is recovering. High volatility = high premium on every contract I sell. Earnings April 22.

Planet Labs went from ~$3 a year ago to $35+ — roughly 10× in 12 months. I entered near the top of that move at $36, so I'm slightly underwater. But that kind of momentum creates exactly the implied volatility that makes covered call premiums worth selling. First CC: $90.

Combined, that's $6,800 in total capital deployed across both positions. So far I've collected $277 from APLD over four weeks and $90 from the first Planet Labs covered call — $367 in total premium since I started selling contracts. At my current run rate, I'm targeting up to $200 a week between both positions. That's $10,400 a year — from $6,800 in capital, managed in five minutes a week. Those aren't lottery-ticket numbers, but they're real, and they grow as I reinvest and add positions.

And here's the part that makes this even better: what if the stock prices recover? You're not just collecting premium — you own the shares. APLD dropped from my $32 purchase price to around $25, but it's already recovering and closed at $27.50 today. Every dollar it climbs back reduces my unrealized loss — and every covered call I sell lowers my effective cost basis further. Planet Labs is only slightly down from my $36 entry. The wheel strategy doesn't require stocks to moon. It just requires them to stop going down — and then it starts working in multiple directions at once.

This is what separates the wheel strategy from pure income plays like savings accounts or CDs. Your capital isn't just sitting there earning interest. It's working — generating weekly income and potentially growing in value at the same time.

What I'm watching next: Hut 8 (HUT). At $52.66 at the time of this writing, it's just above my usual under-$50 threshold — but not by enough to rule it out. Hut 8 is a Bitcoin mining and high-performance computing company with the kind of volatility that generates meaningful weekly premiums. I'm currently researching it as my next position. As I find new tickers that meet the bar, I'll share them here on this blog. Part of running this business is constantly scouting for the next opportunity — just like any business owner would.

The Real Math — Week by Week

I'm a programmer. I like data. So let me show you exactly what happened with APLD — not a hypothetical, the real thing.

I bought 100 shares in mid-February at around $32/share ($3,200 total). The stock started dropping almost immediately. I made a deliberate choice not to sell covered calls right away — the premiums available at strikes above my cost basis were too thin, and I wanted to understand the stock's behavior before committing. That patience cost me some early income, but it kept me from locking in a bad position.

After a few weeks I started selling weekly covered calls. Here's the last four weeks, exactly as they happened:

$277 in four weeks from a $3,200 position. I'm not hitting $200 a week from these two yet — I've been deliberately conservative the last couple of weeks, choosing strikes far enough out-of-the-money that I'm unlikely to lose the shares to assignment. That means less premium per contract, but it keeps me in the trade. I added Planet Labs and collected $90 in the first week there too. Total across both positions: $367 and counting. At a realistic pace, $100 per week per stock is achievable — that's $200 a week, $10,400 a year, from $6,800 in capital. The income is real. It just takes patience to build.

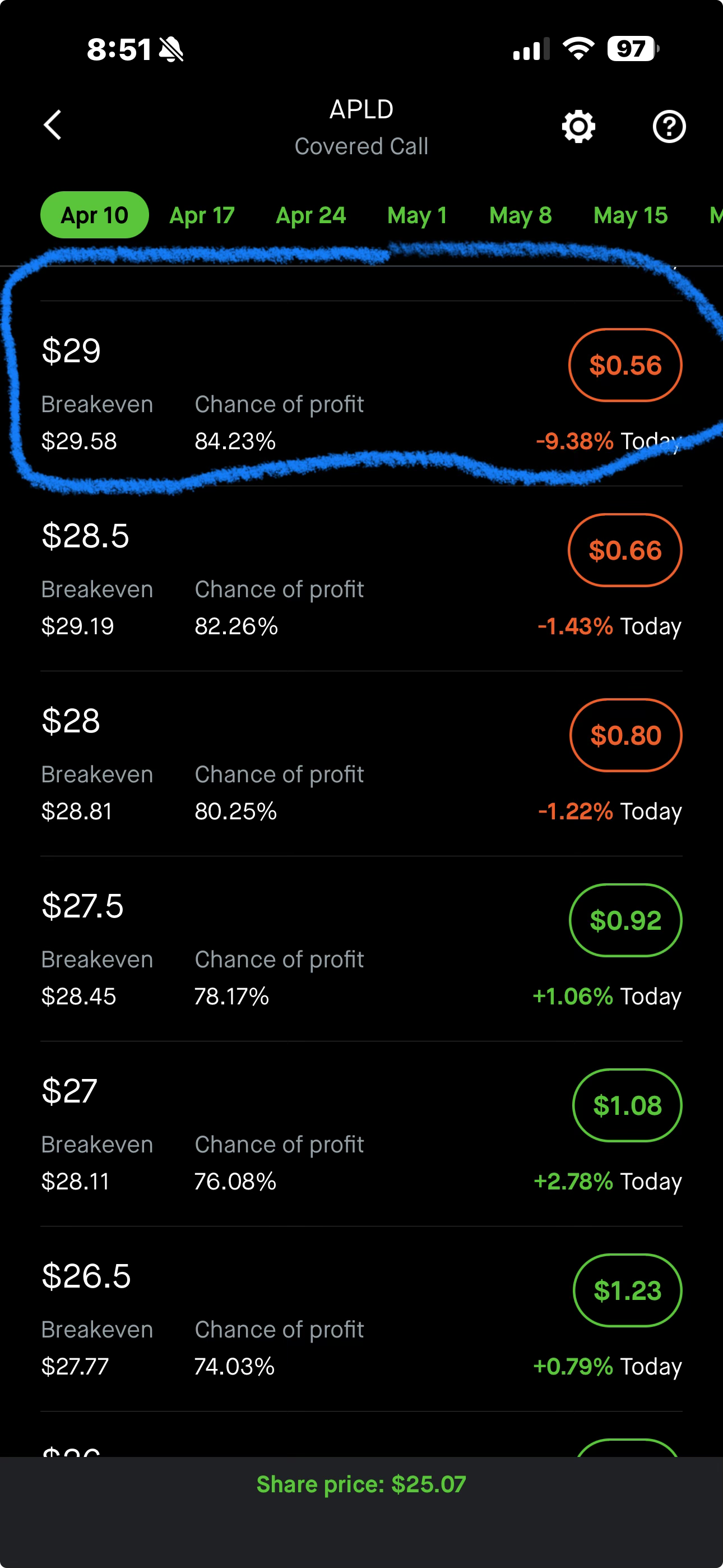

Here's what actually selecting a covered call looks like in Robinhood. This is the real options chain I was looking at for APLD — one-week expiration, Apr 10:

= $56 per contract

(15.7% above price)

The $29 strike is $3.93 above the current share price — deep enough out-of-the-money that there's an 84% chance it expires worthless and I keep the full $56. That's the tradeoff: safer strikes pay less. I choose based on where I think the stock won't go in the next 7 days.

Now here's how that compares to other things you could do with $6,800:

The honest caveat: the stocks can drop. Significantly. If the market crashes or one of your picks has a bad earnings report, you could be holding shares at a loss for weeks or months. This is real investing with real risk. I'm not going to pretend otherwise.

I lived this with APLD. I bought in at $3,200 and watched it slide all the way down to around $2,100 — a loss of over $1,100 on paper, roughly 35% of what I paid. That's not a rounding error. That's real money sitting in the red, and it's uncomfortable in a way that no blog post can fully prepare you for. The harder problem was the strike selection: when a stock drops that far, every strike that generates meaningful premium is dangerously close to where the stock is already trading. Pick too low and you get assigned at a price far below what you paid. Pick too high and you collect almost nothing. I found myself second-guessing the whole idea.

I'm not going to pretend I was calm about it. I thought I'd made a mistake. But I stayed patient, kept selling conservative strikes to protect the position, and the stock has since recovered to $27 a share. I'm still down from my entry, but the gap is closing — and every covered call I've sold along the way has been chipping away at my cost basis. Where it goes from here, I genuinely don't know. That's the honest answer. But walking away at the bottom would have locked in the loss and thrown away everything the premiums were working to recover.

But the premiums cushion the downside. Every dollar of premium you've collected lowers your cost basis. And you're choosing stocks you've researched and believe in — just like any business owner bets on their business. You're not gambling. You're deploying capital with a plan.

Why AI Can't Take This From You

Let me be direct about something. I build AI systems for a living. I see what these tools can do. And I'll tell you honestly — the next three to five years are going to be difficult for knowledge workers.

Programming, design, writing, data analysis, customer support — all of it is being automated faster than anyone predicted. The tools aren't perfect yet, but they don't need to be. They just need to be good enough that one person can do the work of three. When that happens, two people lose their jobs. That's not speculation. It's already happening.

Labor-based income — whether it's a W-2 salary, a freelance contract, or a gig app — is fundamentally vulnerable. If a machine can do your work faster and cheaper, your income is at risk. Doesn't matter how good you are. Doesn't matter how many years of experience you have. The economics don't care about your resume.

Capital-based income is different.

AI can't replicate your brokerage account. AI can't take your shares. AI can't collect your premiums. The wheel strategy runs on two things: capital and a simple weekly decision. The decision takes five minutes. The capital does the rest.

I'm not saying quit your job. I'm saying build something alongside it that doesn't depend on your employer's opinion of your value. Something that runs on what you own, not what you do. Something that keeps generating income whether you're employed, unemployed, or retired.

My programming job funds the capital. The capital generates the income. And if the programming job goes away, the income doesn't.

That's not a side hustle. That's a safety net made of cash flow.

Why I'm Journaling This Publicly

Starting with my next post, I'm going to document my actual trades here on this blog.

Every position. Every premium collected. Every assignment. Every call-away. Real numbers, real tickers, real outcomes — nothing cherry-picked.

You'll see exactly what I'm selling each week, the strikes I'm choosing, the premiums I'm collecting, and whether the trades work out or blow up in my face. You'll see the wins and the losses. You'll see what a good week looks like and what a bad week looks like.

I'll also be sharing new stocks I'm researching — tickers that meet the criteria of being under $50, offering weekly options, and having enough volatility to make the premium worth the risk. If I find a good one, you'll see it here before I see it mentioned on CNBC.

Think of it as a small business owner publishing their books. Full transparency. Here's what I deployed, here's what I earned, here's what I learned.

Why am I doing this? Because most options content out there is theoretical. Hypothetical examples with made-up tickers and round numbers. I want to show you what this actually looks like — week after week, with real money on the line. If the strategy works, you'll see the proof. If it doesn't, you'll see that too.

This isn't financial advice. I'm a computer programmer documenting how I run a small business. You can follow along, learn from my experience, and decide if this model works for you.

What You Need to Start

If you're still reading, you're probably wondering what it takes to actually do this. The barrier is lower than you think.

- Startup capital. You need enough cash to buy 100 shares of your chosen stock. I started with $3,200 for APLD and added $3,600 for Planet Labs — $6,800 total. You can start with just one stock and one contract. Scale from there as your premiums grow.

- A brokerage account with options approval. Fidelity, Schwab, E*TRADE, Robinhood — most major brokers will approve you for Level 1 or Level 2 options trading within a day or two. Covered calls and cash-secured puts are considered basic strategies. You don't need advanced approval.

- Basic understanding of puts and calls. You don't need to be an expert, but you need to understand what you're selling. This article gives you the foundation. I'll be publishing more detailed guides in the coming weeks.

- A way to track your trades. This is where most people lose visibility. You sell a put, it expires, you sell another, you get assigned, you sell a call — and suddenly you have no idea if you're actually making money or just staying busy. If you don't know your P&L, your win rate, your average premium, and your projected annual income, you're running a business without looking at your books. You wouldn't run a laundromat without tracking revenue and expenses. Don't run this business without tracking your premiums and grades.

How I Track It All

When I started wheeling, I tracked everything in a messy spreadsheet. Formulas broke. I lost track of which puts turned into assignments. I couldn't tell if my trades were actually good or just lucky. I was making money but flying blind.

I'm a programmer, so I did what programmers do — I built something to fix it.

Premium Tracker is a free Google Sheets add-on I created specifically for wheel strategy traders. It auto-calculates your P&L across the entire lifecycle of each position — open to close in a single row. It grades every closed trade with a 7-factor scoring system, giving you a letter grade (A through F) and a 0–100 score so you know exactly how well you executed. It projects your annual income based on your real performance, not a back-of-the-envelope guess. And it gives you a dashboard — YTD income, win rate, average grade, top tickers — updated every time you refresh.

If you're going to run this as a business, you need to know your numbers. Premium Tracker gives you that — for free.

The journal entries I'm publishing on this blog will show Premium Tracker in action. You'll see the grades, the scores, and the dashboard as I document my trades week after week.

The Boring Business That Changed My Mind

I almost bought a vending machine. I'm glad I didn't.

I'm a programmer watching AI reshape my entire industry. I could panic about that. I could ignore it and hope for the best. Or I could build something that doesn't depend on my job title, my employer, or the market rate for code.

I chose to build.

The best small business doesn't require a lease, a loan, employees, or a buyer when you want out. It requires capital, a strategy, and a few minutes a week. The wheel strategy isn't glamorous. There's no storefront, no grand opening, no Instagram-worthy office. But it generates real income, it scales with reinvestment, and it runs while you sleep.

Start small. Buy 100 shares of something you believe in. Sell one covered call. See what happens.

I'll be documenting every move right here. Follow along — and bring your spreadsheet.